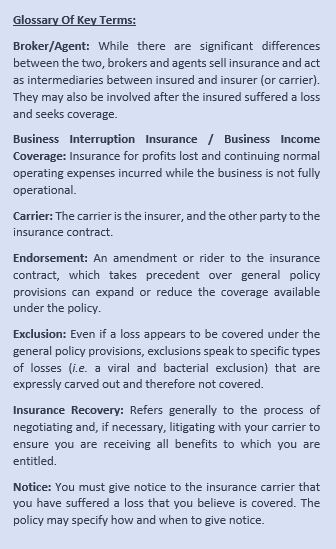

In the wake of COVID-19, businesses everywhere are reckoning with how to keep dollars coming in the door. While many will find that coronavirus itself will not trigger insurance coverage, every impacted business should be taking a hard look at their existing policies. Business should consider the following five steps to better their position with regard to their existing insurance policies. For those who are unfamiliar with insurance coverage issues, a glossary of key terms is included. For those looking to dig deeper, read on for a more substantive discussion of the key provisions and issues that may arise, as businesses attempt to secure coverage for losses caused by COVID-19.

In the wake of COVID-19, businesses everywhere are reckoning with how to keep dollars coming in the door. While many will find that coronavirus itself will not trigger insurance coverage, every impacted business should be taking a hard look at their existing policies. Business should consider the following five steps to better their position with regard to their existing insurance policies. For those who are unfamiliar with insurance coverage issues, a glossary of key terms is included. For those looking to dig deeper, read on for a more substantive discussion of the key provisions and issues that may arise, as businesses attempt to secure coverage for losses caused by COVID-19.

FIVE-STEP INSURANCE COVERAGE CHECKLIST:

- Review all existing insurance policies, front to back. One-page endorsements tucked in the back may dramatically change what sort of claims are and are not covered by the policy.

- Do not rely too heavily on the advice of your broker or agent. Your broker or agent may attempt to negotiate claims between you and your carrier. Communicate with your broker or agent, ask for their advice, but know that they may have conflicting incentives.

- If in doubt, give notice to your carrier about the loss. Failure to give notice can result in waiver of coverage that you otherwise might have.

- Meticulously document both the cause and amount of any losses. For example, if a key supplier says they need to back out of an agreement due to coronavirus, ask follow-up questions and take detailed notes.

- Consult an attorney who has experience negotiating with and litigating against carriers.

BUSINESS INTERRUPTION. Some businesses may find relief in their existing business interruption insurance (or business income coverage). This coverage arises most commonly with a fire or natural disaster that destroys a building. Ideally, the business would turn to first-party property insurance for construction costs, while seeking business interruption coverage for the business income that was lost while the building was unusable. As stated by one Wisconsin court, “[b]usiness interruption insurance covers profits lost and continuing normal operating expenses incurred while the business is not fully operational.”[i]

If your business has a general property or commercial policy, it likely has some form of business interruption coverage. But just because the coverage is part of the policy, it does not follow that you will be entitled to reimbursement any time you suffer a loss of business income. There must be a covered loss to trigger the business interruption coverage. An insurance policy is a contract and the existence of insurance coverage turns, first and foremost, on the policy language and the nature of the insured’s losses.

PROPERTY DAMAGE. The most common trigger for business interruption coverage is physical damage to the insured’s property. Property damage often involves damage that structurally alters the property (like a fire or floods) so courts may be skeptical of claims that coronavirus constitutes property damage. Nonetheless, some courts have held that, even in the absence of visible damage, physical damage can be established by showing that the insured property was rendered unusable or uninhabitable.[ii] For example, a federal court in Oregon has stated that “physical damage can occur at the molecular level and can be undetectable in a cursory inspection.”[iii] Once again, whether coronavirus constitutes physical property damage will hinge on the policy language used, and the ways in which the virus impacts the insured’s business.

Moreover, even if coronavirus does not itself cause physical loss, it could lead to property damage. For example, with millions of employees shifting to remote work, there may be no one around the insured’s property to notice a plumbing leak before it causes significant water damage. Similarly, with no employees present, the insured’s property may become a target for a burglary. If the insured loses key equipment or hardware, it may cause an interruption in business.

CIVIL AUTHORITY. A somewhat common trigger to business interruption coverage involves closure by order of a “civil authority” such as a city or state agency. Civil authority coverage may still require property damage—for example damage to a nearby building, which leads a government authority to bar access to the entire block. However, the policy language varies, and the opportunity to secure coverage via civil authority orders will continue to grow, as agencies become more proactive in attempting to control coronavirus.

CIVIL AUTHORITY. A somewhat common trigger to business interruption coverage involves closure by order of a “civil authority” such as a city or state agency. Civil authority coverage may still require property damage—for example damage to a nearby building, which leads a government authority to bar access to the entire block. However, the policy language varies, and the opportunity to secure coverage via civil authority orders will continue to grow, as agencies become more proactive in attempting to control coronavirus.

VIRAL AND BACTERIAL EXCLUSIONS OR ENDORSEMENTS. A policy might provide for exclusions, such as a Virus or Bacterial Exclusion, which squarely preclude coverage caused by coronavirus. Conversely, a policy can explicitly include such coverage through an endorsement. Insureds may have virus or bacterial coverage without realizing it. For example, a business that is highly sensitive to cyber risks may have obtained virus and bacterial coverage as part of a package of endorsements that the insured purchased primarily with the intention of securing cyber coverages.

DIFFERENT COVERAGES. There are other permeations of business interruption insurance that, while less common, provide significant benefits. For example, “contingent business interruption” insurance may provide coverage if a key supplier of the insured suffers property damage, resulting in losses to the insured. A “leader property” endorsement may provide coverage for physical loss or damage to nearby property, where the insured’s business relies upon the neighboring property. As an example, this could come into play for restaurants adjacent to schools or sports stadiums that have been shut down. Finally, an insured may have service interruption coverage for loss to electrical, steam, gas, water, sewer, telephone, or other utilities, should those situations arise.

OTHER FACTORS. Assuming coverage exists, there will be several additional factors to consider and negotiate with the carrier. Coverage may be limited by time period (i.e. two weeks after a civil authority imposes an order) or dollar value (i.e. only the first $50,000 of lost business income). The insured will also be expected to prove its losses and should therefore meticulously document both the cause and extent of any losses. The insured should also be mitigating damages. The insured will be expected to take reasonable steps to minimize its business interruption (by, for example, emphasizing online sales, if possible).

CONCLUSION. Policy language varies greatly and COVID-19 is largely unprecedented. No business should assume that they are without coverage. Follow the Five-Step Insurance Coverage Checklist and contact one of the authors if you need assistance in evaluating your policies.

Rathje Woodward routinely advises insured companies on how to maximize their insurance coverage. Rathje Woodward negotiates claims with carriers and, where necessary, litigates coverage disputes through to trial and appeal. Rathje Woodward’s attorneys also have extensive experience in commercial litigation, employment, business and government law, among many other areas.

Rathje Woodward LLC advises clients on a broad range of insurance coverage issues. RW negotiates claims with carriers and, where necessary, litigates coverage disputes through to trial and appeal. RW’s attorneys also have extensive experience in commercial litigation, employment, business and government law, among many other areas. If you have questions about insurance coverage issues, contact our office at 630-668-8500. Our online contact form may be found here.